Expat tax services from trusted tax experts

Why work with Taxes for Expats

Deep expertise

Personalized service

Exceptional accuracy

-

![Americans at home and overseas]()

Americans at home and overseas

-

![Dual citizens with US passports]()

Dual citizens with US passports

-

![Americans behind on US taxes]()

Americans behind on US taxes

-

![Green card holders]()

Green card holders

-

![American retirees abroad]()

American retirees abroad

-

![Non-US citizens with US tax duties]()

Non-US citizens with US tax duties

-

![Accidental Americans]()

Accidental Americans

-

![Digital nomads]()

Digital nomads

-

![Businesses required to file US taxes]()

Businesses required to file US taxes

-

![Not a typical filer?]()

Not a typical filer?

Schedule a call

Trusted by 50,000+ clients

Mentioned in

How we work

Expert, human accountant working on your case

Professionals who care & stand ready to answer your questions. Experienced humans who understand expat taxation in and out.

80+ accredited CPAs, EAs, JDs.

Real people, just like you.

50,000+ clients, 193+ countries, 4,000+ reviews

Frequently asked questions

At Taxes for Expats, we help individuals and businesses with US tax obligations, including:

- Americans living in the US or abroad

- Dual citizens with US passports

- Green card holders

- Accidental Americans

- Non-US citizens with US tax requirements

- Digital nomads

- US retirees living overseas

- Businesses with US tax requirements

No matter your situation, our team has the expertise to guide you through your US tax filing with confidence.

We offer Federal Income Tax Return and Expanded Income Bundles tailored to your specific tax filing needs. For a detailed overview of our fees, please visit: Our Fees.

To find out which documents and information are required for your tax preparation, please check our guide here: Tax Documents Needed.

Yes, we stand behind the work we do. If the IRS questions a return prepared by us, we will review the letter and advise you on the necessary steps. For more information, see: Received IRS Letter.

We offer free support via phone, email, and chat. For more information on our support options, please visit: Support Options Overview.

Absolutely. TFX has been preparing US expat taxes for over 25 years and is well-versed in the tax laws applicable to US expats worldwide.

Absolutely! If you’re a non-US citizen with US tax obligations – whether due to income earned in the US, business dealings, or other connections – we can help. Our team understands the complexities involved and will guide you through the necessary filings with ease.

We prepare a wide range of forms, including 1040/1040NR, Form 5471, Form 5472 with Form 1120, and many more. For a full list of forms we handle, please visit: Forms We Prepare.

Yes, we can file an extension for you at no additional cost. However, we require a $50 retainer, which will remain as a credit on your account for future TFX services.

We only work with seasoned CPAs or EAs who each have at least a decade of experience in the field. We don’t employ junior staff.

Our goal is to complete each tax return within fifteen (15) business days per filing year. We prioritize quality and accuracy, with every return undergoing a thorough review by both a preparer and a supervising CPA or EA.

If you're unsure whether you need to file US taxes, we can help you determine your filing requirements. Even if you're living abroad or have limited US ties, you may still have an obligation to file. We’ll review your specific situation and provide personalized guidance.

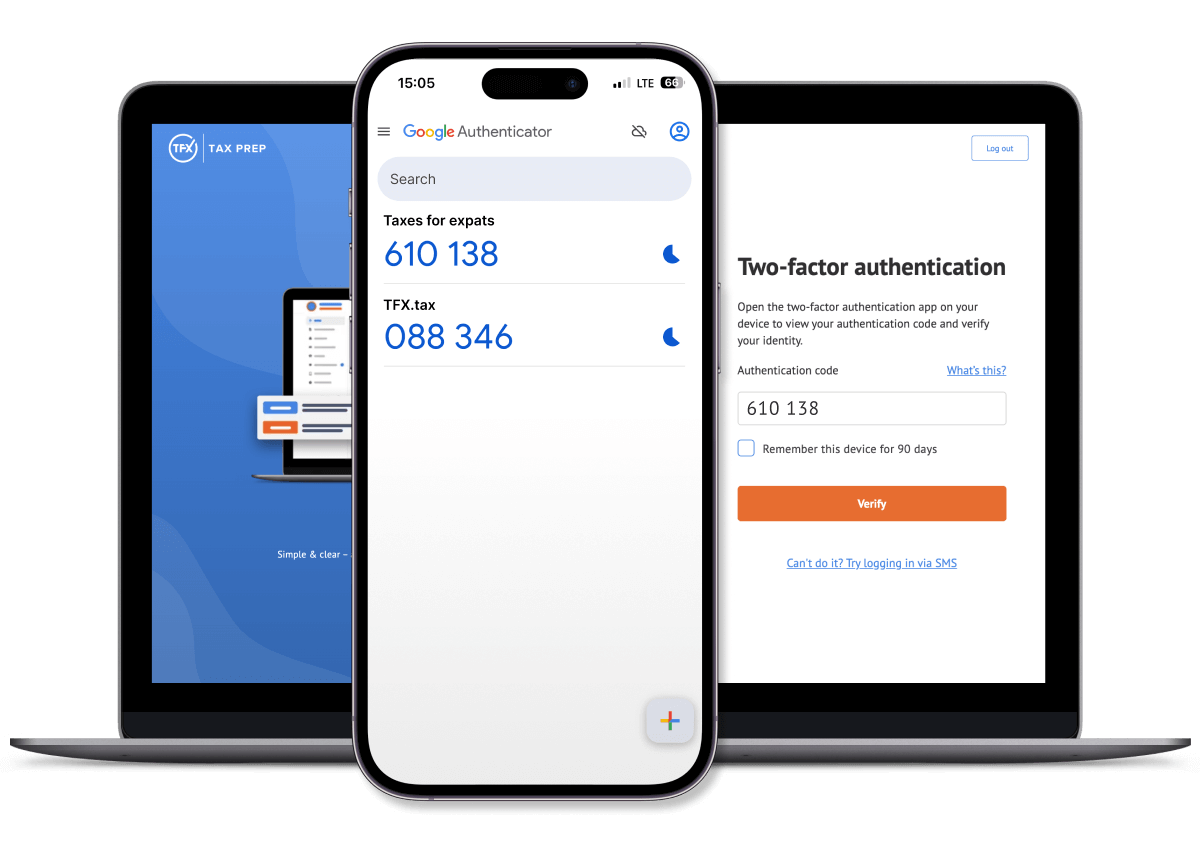

Top-tier security protocols to protect your information

All sensitive data is encrypted at rest and in transit using cutting-edge encryption protocols (AES-256). For added protection, we implement two-factor authentication (2FA), delivering an extra layer of security to safeguard your information against unauthorized access.

Articles & tax guides

View all →What is Form 14653? Form 14653 is the IRS certification form u...

The Internal Revenue Service introduced the ...

Viele Amerikaner, die in Deutschland leben, stellen Jahre später fest, dass von ihnen immer noch erwartet wird, US-Steuererklärungen abzugeben, ausländische Bankkonten zu melden und die internationalen Meld...

“I am completely at ease now – TFX made it very easy, and going through the Streamlined Procedure made everything that came after simpler too." Jonathan Balseca, occupational doctor, Ecuador Jonathan Balseca, an occupational doctor in Ecuador, holds US...

Your 401(k) usually stays open when you move abroad, and a US citizen does not become a foreign payee just because of a foreign address. The real changes are practical and tax-related: employer-plan access, future contrib...

US citizens and resident aliens abroad must report foreign self-employment income on a US tax return when they meet the filing rules for the 2025 tax year. The key issue is that self-employment tax on foreign earned income is separate from income tax, even when the Foreign Earned Income Exclusion (FEIE) reduces taxable income on Form 1040. ...

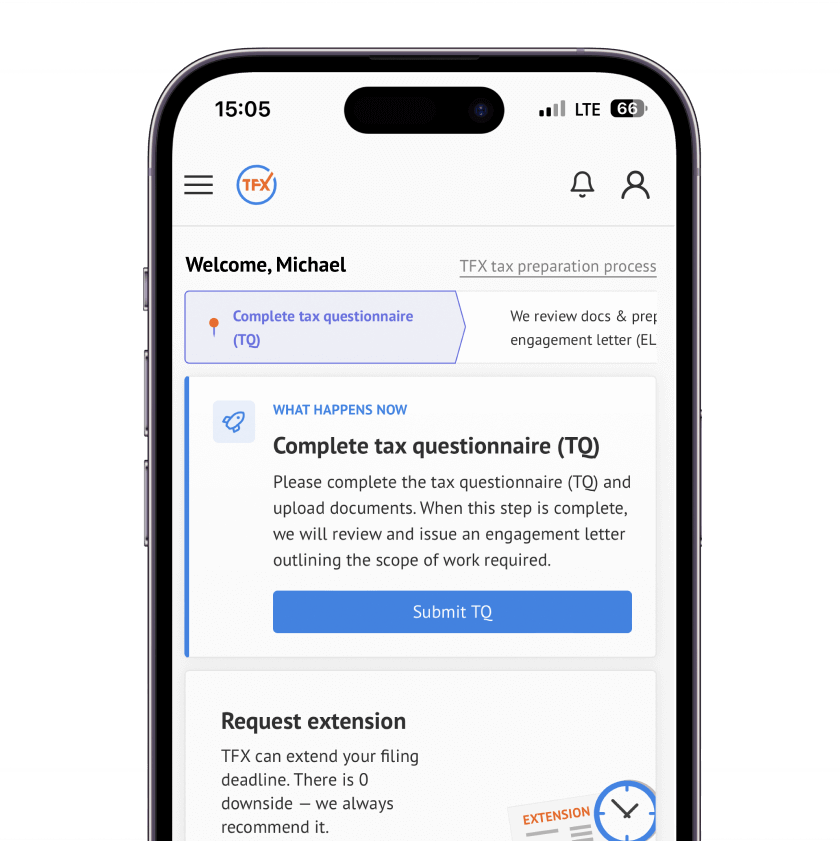

All your important information at your fingertips!

Our platform combines all your data into one personalized dashboard for unmatched convenience and efficiency.